Reconstructing Ukraine at war: The journey to prosperity starts now

TABLE OF CONTENTS

Introduction

Section 1: Summary of damages and the economic and financial situation

Section 2: First steps toward building a reconstruction strategy

Section 3: Steps to create a reconstruction-friendly ecosystem

Section 4: The best opportunities for each economic sector

Summary of recommendations

Conclusion

WATCH THE LAUNCH

Introduction

Rebuilding the Ukrainian economy after years of war will be a monumental task that the country’s allies and partners know they must assist. Helping Ukraine to prosper should be just as big a priority for those who believe Ukraine’s victory is key to preventing further Russian aggression and sending a cautionary message to other autocrats around the world. While rarely dismissed out of hand, the reconstruction is intuitively seen by many in the West as secondary to the need to help Ukraine fight back against aggression. This is understandable, but neglects how reviving the Ukrainian economy—and the government’s cash flow—also helps the war effort through additional funds, resources, and motivation.

The Ukrainian government is staffed by clever, innovative experts capable of expressing a clear vision of how to reach prosperity. But when the Atlantic Council’s Global Energy Center and GeoEconomics Center embarked on a weeklong research trip in February 2024 to meet them, Kyiv faced cash-flow problems and high uncertainty over future macrofinancial assistance, especially from the United States.

The situation has since improved, not least thanks to the US supplemental spending law that includes $10 billion of budgetary support—but it’s imperative that the West does not create doubts about its support for Ukraine again in 2025. The macrofinancial assistance meant to keep Ukraine’s government functioning cannot finance the recovery as well. In addition to central government funds, a myriad of Western grants and loans need to be tied to individual projects. The innovative systems designed to implement this are up and running but not always used to their full potential.

This report provides a snapshot of the economic, societal, and energy-security situation on the ground, capturing key challenges and opportunities for supporting Ukraine’s survival and building a more prosperous future. It also explores how the country can meaningfully contribute to Europe’s economic growth and strategic autonomy at large through innovation, energy security, decarbonization, and diversified supply chains. While the situation is changing daily, these key takeaways will remain pertinent to reconstruction discussions for the foreseeable future.

Our research is based on more than thirty meetings in Kyiv in February 2024. These included meetings with the most senior levels of the ministries in charge of reconstruction, influential think tanks, Western embassies, legislators in the Rada, journalists, and business leaders. These meetings were conducted under the Chatham House Rule. Our trip was followed by additional visits to Ukraine by the Atlantic Council Eurasia Center in February and March. With further research and follow-up discussions with experts, we have summarized our analysis in this recommendations-focused Atlantic Council report.

Section 1: Summary of damages and the economic and financial situation

Taking stock of unexpected wins and measuring sobering losses

Moscow’s relentless assault has caused immeasurable humanitarian suffering and damage to Ukraine’s infrastructure and natural environment. Since the Russian Federation’s 2022 invasion of Ukraine, more than 14.6 million Ukrainians, or a third or more of the population, have fled their homes at some point during the war, according to the International Organization for Migration (part of the United Nations system); 6.5 million refugees fled Ukraine, and 3.7 million are still displaced within the country. By February 2024, at least thirty-one thousand Ukrainian troops and tens of thousands of civilians have died for reasons related to the war. And while the Ukrainian army succeeded in pushing the Russian aggressor far back in 2022, physical damage is by no means limited to the front line. As of February 2024, 156,000 square kilometers (km) in liberated territories and along the active front have been contaminated with mines, which were rarely used before this full-scale invasion. The June 2023 destruction of the Kakhovka dam caused $14 billion in damage and loss, submerged at least 620 square km of territory under Ukrainian control, and damaged ecosystems even further afield. Russia’s air campaigns continue to target the whole country, undermining both the economic recovery and morale.

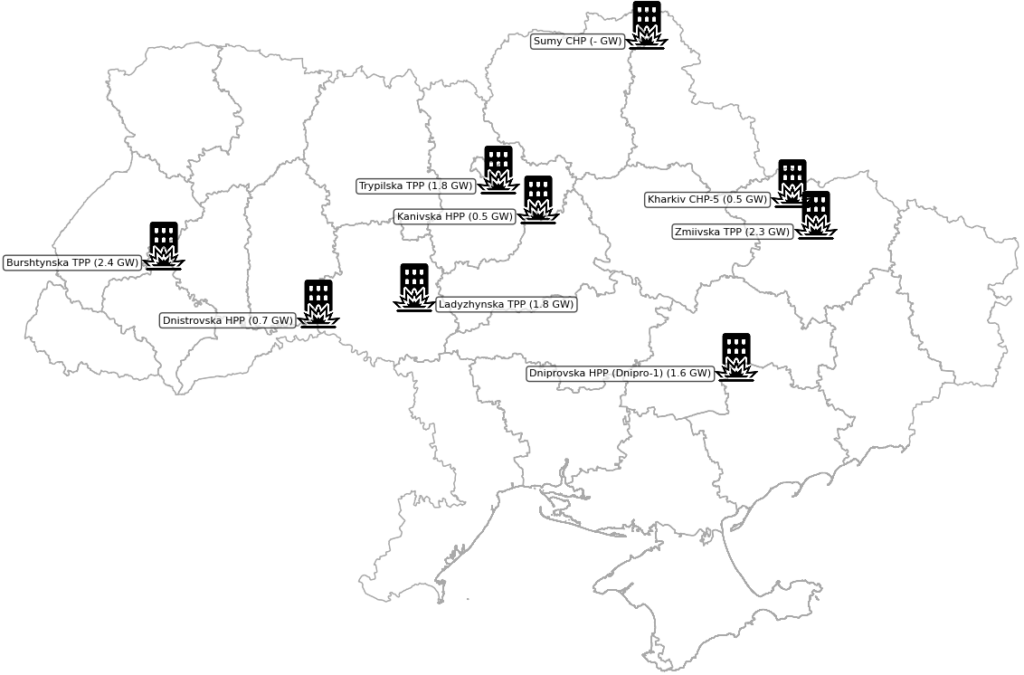

Targeting energy infrastructure has been one of Russia’s most pernicious and persistent tactics to cause harm to millions at once and multiply the cost of reconstruction. With over $10 billion in damage to date, these attacks have hindered access to basic human necessities, such as potable water and heating. The international donor community has consistently helped Ukraine with repairing the damage, which was mostly focused on energy generation capacity and transmission in the winter of 2022 and 2023. Thanks to robust international support and the courage and dedication of energy-sector employees, Ukraine survived these horrific months, restoring over 2.2 gigawatts (GW) of installed capacities. Unfortunately, worse was on the horizon. The Kremlin escalated its critical infrastructure destruction starting in March 2024 by bombing Ukraine’s biggest thermal power plants: the heart of generating capacity for the largest population hubs. Delays in military support hamstrung Kyiv’s high-precision defense capabilities, leaving million-dollar power plants exposed to Russia’s hybrid attacks. During the spring of 2024, Ukraine lost 9 GW of generation capacity, which is equivalent to 22 million photovoltaic (PV) panels, or power for 7 million households.

This leaves Ukraine with expensive solutions and a tough journey ahead. The country is left to purchase electricity imports from European neighbors, which are more costly than what it could have produced at home and leads to higher fees due to the oversubscribed transmission capacity. It costs around $0.20 per kilowatt-hour to produce electricity in Ukraine. Households paid a fraction of this after subsidies, which are being incrementally reduced in an effort to bring in additional funding to repair the damages, resulting in $0.107 per kilowatt-hour cost to consumers until April 30, 2025. At the same time, Ukraine and its allies are racing to secure gas turbines for energy generation and balancing needs, as well as parts to repair power plants. Cities are already experiencing blackouts, which will be more frequent when the heat-driven peak summer demand overloads the grids. Ukraine will need a mix of budgetary support, equipment transfers, and technical assistance to survive this winter, which promises to be the most challenging since the full-scale invasion.

Domestic energy availability in Ukraine: 2022-2024

Power plants destroyed in Ukraine as of April 2024

Source: Available data collected by DiXi Group through the following references; Atlantic Council mapping:

- https://www.undp.org/ukraine/publications/towards-green-transition-energy-sector-ukraine

- https://www.ukrinform.ua/rubric-economy/3814073-v-ukraini-vze-vidnovili-22-gvt-potuznostej-poskodzenih-cerez-ataki-rf-smigal.html

- https://interfax.com.ua/news/general/955734.html

- https://biz.liga.net/ua/all/all/novosti/hihantskyi-obsiah-ukraina-za-misiats-vtratyla-7-hvt-enerhoheneratsii

- https://www.undp.org/ukraine/publications/towards-green-transition-energy-sector-ukraine

- https://biz.liga.net/ua/all/all/novosti/hihantskyi-obsiah-ukraina-za-misiats-vtratyla-7-hvt-enerhoheneratsii

- https://expro.com.ua/novini/energoatom-virobiv-476-elektroenerg-v-oes-ukrani-za-7-msyacv-2023r

Efforts to quantify overall damages systematically are important in the pursuit of justice. The Register of Damage Caused by the Aggression of the Russian Federation against Ukraine (RD4U) will be a source of information. Established through a Council of Europe resolution, the register receives, processes, and records claims filed by individuals, entities, and the Ukraine government for damage, loss, and injury from wrongful Russian aggression against Ukraine. (Forty-three nations and the European Union have joined the Register.) A compensation mechanism is yet to be established, but the register is an essential step in the process of pursuing compensation from Russia. The catalog should aid in ensuring that compensation is provided to the right individuals and broader communities. Citizens can now make entries via the Diia app, the main platform for Ukrainian government services.

Three rounds of Rapid Damage and Need Assessments (RDNA) already provide evidence of the mounting toll of the war. The World Bank, the government of Ukraine, the European Commission, and the United Nations coordinate to provide a reliable tally of “total costs” imposed on the Ukrainian economy by Russia’s aggression, with the latest citing direct damage to buildings and infrastructure of up to $152 billion and an estimated recovery and reconstruction cost surpassing $486 billion—“approximately 2.8 times the estimated nominal GDP of Ukraine for 2023.” It is noteworthy that these include the direct cost of destroyed or damaged physical assets and infrastructure—which started increasing significantly as Russia has targeted energy infrastructure—and also economic losses from lost activity and increases in the number of citizens needing assistance. The estimated restoration cost does cause some double-counting alongside the accounting for destroyed physical assets. However, this does not mean the bar for funding the reconstruction is low. The RDNAs integrate the loss of domestic production and increasing dependence on state handouts, which have both reduced revenues and increased liabilities for the government.

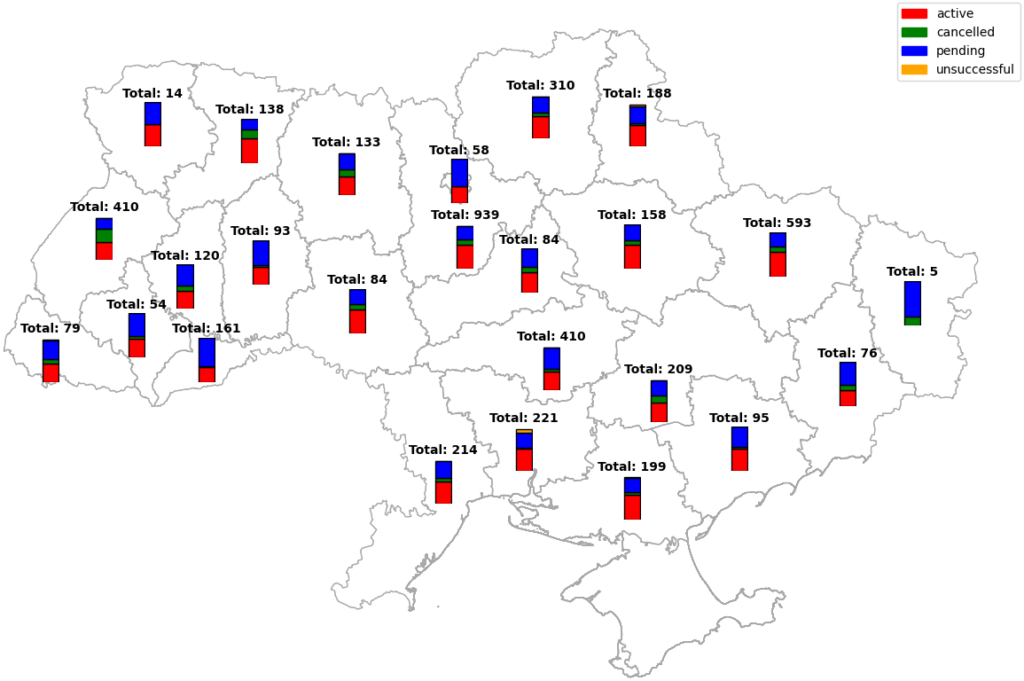

Meanwhile, Ukraine has developed a digital platform to track reconstruction projects in the nation: the Digital Restoration EcoSystem for Accountable Management (DREAM). The platform can help the government and international financial institutions (IFIs) differentiate between large-scale reconstruction projects that are long-term endeavors and short-term urgent repairs, and then orient appropriately. In this regard, DREAM is a rare combination of polyvalence and transparency. Developed in tandem with Ukrainian civil society and with support from USAID and UK Aid Direct, the DREAM platform was launched in 2023 by the Ministry for Restoration (formerly the ministry for infrastructure). DREAM is both a “digital route” for and a “window” into projects repairing or replacing infrastructure damaged by the war. Citizens, firms, and municipalities can submit evidence of damage, receive provisional approval, submit invoices, and receive compensation straight to their bank accounts. The platform is transparent down to every individual project. By mapping their density by region, we can see that restoration projects cover most of the territory controlled by the Ukrainian government, whereas new construction projects remain focused on larger cities.

Status of rehabilitation projects logged in the DREAM portal

Data as of April 2024

Source: Dream.ua data and Atlantic Council mapping.

The large percentage of pending or unfinished projects may be due to improper documentation of requests and, in part, a legacy of the cash-flow issues Ukraine faced earlier this year, and has since improved following Japan’s earlier-than-planned donations, EU “bridge financing” (discussed below), Canadian assistance, and passage of a long-planned $61 billion US aid package. Incomplete or poorly prepared applications also account for some of the backlog: Local governments often input projects to ensure they’re noticed but lack the expertise to perfect their write-ups. Still, it is also noteworthy that projects can still be approved without working through DREAM. Direct commissions of large projects can still, as far as we know, bypass DREAM as well. Of the four major lending institutions, only the European Investment Bank (EIB) is using the system. The Cabinet of Ministers of Ukraine had resolved in 2022 to make the use of the platform mandatory but the relevant law has not yet been adopted.

Finally, the work of civil society in connecting funders, firms, and communities in need remains important. The Kyiv School of Economics’ Recovery Lab and former Deputy Foreign Minister Lana Zerkal, who serves on the Coordinating Committee of the Ukraine Facility Platform, among others, are advancing this work.

The state of Ukraine’s economy and finances

Despite the onslaught of aggression and destruction, Ukraine’s economy is growing: 5 percent in 2023 and, based on the International Monetary Fund’s (IMF) forecasts, another 3 percent in 2024. But this comes after a 29.1 percent drop in 2022 and a large loss in the workforce in 2022 due to the mobilization, but 4.5 million Ukrainians have returned home since then. Still, the IMF does not expect the economy to reach its prewar level of production until 2029, and that relies on an assumption of the war ending in the next year. It would also be wrong to think the domestic economy is truly growing. It is adapting to wartime conditions and new firms are being created, but the amount of budget assistance, recovery funding, and humanitarian aid being sent into the country is the dominant factor.

The resumption of shipping from ports provides a bright spot in terms of exports. Despite environmental damage, a perilous sea route, and protests by EU farmers at overland points of entry, Ukraine’s exports of grain and oilseed products are recovering, reaching a wartime high in February 2024—but have not yet reached preinvasion levels.

Firms with a presence in Ukraine have continued to invest. This is partly in repairs and upkeep, but they are also expanding into new fields to shore up their own supply chains or respond to demand. International firms with an established presence in Ukraine have found demand for their products increasing, especially without Russian competitors and with domestic production capacity damaged. The crucial problem is that greenfield investment (i.e., projects starting from the ground up) has been close to zero.

The following chart compares the different components of the national accounts in constant prices. Three clear phenomena are at play: a significant expansion of government spending, irregular gross capital formation as investment slows and firms run down inventories, and increasing reliance on imports. The overall size of the economy is still noticeably smaller—even in the much-depreciated hryvnia. Were data in the chart in current US dollars, the shrinking of the economy would be even more noticeable.

Ukraine national accounts, constant prices

Government revenue has been volatile, though adaptation to wartime conditions and the knock-on effects of inflation have allowed for an impressive recovery. Excluding grants, government revenues fell to $36 billion in 2022, a 32 percent drop from $53 billion in 2021—but recovered sharply in 2023 to $46 billion and are forecast by the Ministry of Finance to fall slightly to $43 billion this year.

The challenge is that the government is expected to fund the war effort while paying pensions, keeping services running, and contributing to repairs and replacements made necessary by war damage. The 2024 budget forecasts $82.3 billion in expenditures, over half of which will go to the war effort and domestic security. In the budget, spending on repairs and reconstruction will fall under the categories of interbudgetary transfers and economic activity, which make up less than 10 percent, but are not exclusively devoted to these goals, putting the ceiling for centrally organized spending on restoration at less than $8 billion. The numbers in Kyiv’s budget reflect only what goes through the Ministry of Finance, so do not include contributions in-kind or directly to the local governments.

Ukraine already faces a large foreign-currency debt burden which it is trying to honor. For now, an agreed holiday on interest payments and war uncertainty preclude it from borrowing more on international markets. So the budgetary deficit has to be filled with a combination of international assistance (both grants and loans) and domestic bonds. Since the beginning of the full-scale invasion, $25 billion in domestic bonds have been purchased; the Ukrainian government would rather not have to rely on bonds too much as domestic savings are finite and the financial system also needs liquidity. Ukraine received $42.5 billion in external financing last year and is on track to receive about $38.6 billion in financial assistance in 2024.

Kyiv has tried to stick to certain principles to remind donors that it is treating their support with care. Its tax revenues cover defense spending, excluding donated equipment and other logistical and intelligence support. Grants and loans from friendly governments and IFIs cover the rest of the government’s liabilities. Kyiv also likes to remind supporters that it is engaging heavily with its bondholders ahead of the end of the debt holiday, which is currently set to end in August 2024. Negotiations with a consortium of Eurobond holders are currently revolving around a resumption of regular payments in exchange for forgiveness of an unspecified chunk, whereas governments that have lent to Ukraine have agreed to holidays lasting until 2027. This is a delicate negotiation for Kyiv, which has avoided falling into “default” status thus far but may do so this year even if bondholders agree to a haircut. The government also has managed to satisfy the IMF that its fiscal consolidation efforts are genuine, as the National Revenue Increase Strategy, published in late 2023, unlocked an $880 million tranche of IMF loans, with an additional $2.2 billion expected in June.

The National Bank of Ukraine (NBU) deserves credit for stabilizing and running a fully functioning financial system, even at the very start of the full-scale invasion. High interest rates and strict controls have prevented capital flight and allowed exchange rates to stabilize following a planned devaluation in July 2022, which reflects lower growth potential and higher dependence on imports. On the other hand, remittances and charity donations—in addition to Western aid—have helped to keep hard currency flowing into Ukraine and prevent a balance-of-payments crisis. The NBU has managed to recover and even surpass the reserve position it had before February 2022. To encourage investments, the NBU has recently announced the relaxation of controls on the payment of dividends to foreign investors and the repayment of foreign currency loans, albeit under a monthly cap.

The goal of this first section was to show the extent of the damage to the Ukrainian economy and that, even with national resilience and competent management, Russian efforts to inflict further devastation continue and the economy still relies absolutely on external support. In the next section, we will look at how this external support is being organized and how this can be improved, both to accommodate bigger strategic decisions alongside day-to-day spending and to demonstrate to Russia that Kyiv won’t run out of money.

Section 2: First steps toward building a reconstruction strategy

Building a reliable flow of money

Ukrainians and the international donor community must be unified around the vision for and the approach to Ukraine’s reconstruction to ensure efficient resource utilization and impactful collaboration. Given the destruction of significant parts of its energy system, industrial base, and housing stock, the country will have to balance urgent basic humanitarian needs with large-scale economic transformation.

First and foremost, Ukraine needs financial and military assistance to be as reliable as possible for at least the next five years to demonstrate long-term resolve to its people and to the Russian leadership. Such steadiness would also provide a more predictable environment for investors, whose decisions to bet on Ukraine’s future will accomplish part of the reconstruction aims and reduce dependence on outside support. Postponements and delays, on the other hand, risk entrenching population displacement and investor reticence.

UK Foreign Secretary David Cameron recently promised that the United Kingdom would give £3 billion a year “for as long as it takes.” Other governments should consider communicating on their commitments in as simple and clear a way, though the political consensus on supporting Ukraine isn’t always as clear as it is in the UK, where the Labour Party has also pledged “ironclad” support for Ukraine in its battle against Russia. Other countries such as Canada, Spain, and Belgium have done the same on military aid, albeit with lower financial commitments.

Passed in early 2024, the European Union’s €50 billion Ukraine Facility is meant as an integrated strategy. The best-publicized part, pillar one, covers €17 billion in grants and €33 billion of loans from 2024 through 2027. The first disbursement—€4.5 billion of “bridge financing”—was sent on March 1. The facility’s innovation comes with pillars two and three. Pillar two provides derisking mechanisms for investors via a “Ukraine Guarantee” of €6.97 billion covering risks for loans and other credit instruments offered by IFIs such as the European Investment Bank (EIB) and the European Bank for Reconstruction and Development (EBRD). Pillar three offers technical assistance to help Ukraine converge with EU rules and prepare for accession. The facility also is remarkable for including minimum targets of green projects and tasking the EIB with working with subsovereign entities like regions and municipalities.

Other governments have made an extra effort at decisive moments to help Ukraine. G7 finance ministers’ meetings are the main venue for where Kyiv’s macro financial assistance needs are discussed. For example, as Ukraine’s cash flow problems mounted early this year amid a delay in US assistance and the impact of farmers’ and truckers’ protests on Ukraine’s exports, Japan was able to accelerate a donation of just under half a billion dollars to February, allowing Kyiv to pay teachers’ and other civil servants’ salaries in March and April. This was coordinated through the G7. Canada also sent two billion Canadian dollars through a concessional loan in March, the same day that the third review of the IMF program was completed.

Recovery funding now benefits from its own coordinating body, the Multi-agency Donor Coordination Platform. Launched in January 2023, the body is supported by a Brussels- and Kyiv-based Secretariat. The permanent members of the Steering Committee are Ukraine, the EU, the United States, and the other Group of Seven countries. In February 2024, the roster expanded to include the Republic of Korea, Netherlands, Norway, and Sweden as temporary members, who either have contributed or are committed to contributing at least 0.1 percent of their country’s 2022 GDP and at least $1 billion. Six EU members have observer status: Denmark, Estonia, Latvia, Lithuania, Poland, and Spain. IFIs participate in the meetings.

Already, the Multi-agency Donor Coordination Platform is becoming more prominent. The most recent meeting took place in Kyiv and the US deputy national security advisor for international economics, Daleep Singh—one of the architects of the Russian sanctions regime—made the trip.

The expansion of participants in this coordinating body isn’t sufficient to secure the volume of assistance that Ukraine needs. At its current level of intensity, the war entails an active front that has to be manned, with frequent air raids on civilian infrastructure and valuable economic targets. The flow of aid to Ukraine needs to be sufficient to keep government services operating while funding appropriate repairs within a reasonable time frame.

The two priorities are of course funded by different types of Western support: macro financial assistance funds the Ukrainian government and keeping services open while the recovery would ideally be funded through recovery loans but these haven’t been fully disbursed because they haven’t been matched with enough projects. To avoid delays and inefficiencies, Kyiv should continue building out trust and transparency mechanisms to showcase how international support is deployed. Large in-kind donations such as spare turbines and transformer equipment have been useful on occasion, but come with costs, from transportation to adaptation for the local infrastructure. Some urgent needs are best addressed with cash transfers, which donors are still uncomfortable providing to organizations in certain sectors, like energy.

Money is fungible and the lack of macro financial assistance earlier this year did force the Government of Ukraine to defer recovery projects, though these in theory are funded from a different source. An improvement the Multi-agency Donor Coordination Platform can make is to apply the coordinating prowess G7 finance ministers have demonstrated on macro financial assistance and do more to bring the flow of recovery funding closer to what the Government of Ukraine and the latest RDNA agree is the budget necessary to tackle recovery priorities—$15 billion this year—and should continue to do so in the years to come.

The Multi-agency Donor Coordination Platform may come across as a simple capital-to-capital device that will entrench centralization. However, its structure in no way precludes the sort of country-to-city or country-to-region donor engagement that has been very successful, albeit on a small scale so far. Led by the Danish Export and Investment Bank, the Denmark-Mykolaiv Partnership has earmarked more than $100 million for reconstruction across the city. Local engagement fosters a timely and needs-based pipeline for aid. In the case of Mykolaiv, Denmark rapidly responded to needs including water purification, wildfire containment, agriculture projects, schools, technical support, and energy infrastructure. Such a partnership enables a city- or region-level focus at times when most of the aid is moving through centralized channels in Kyiv (a necessary but imperfect method for addressing urgent needs in localities). Italy and France are exploring similar partnerships and can draw on vital best practices from the Denmark initiative, such as strong governance and robust stakeholder engagement.

If every European country adopted a Ukrainian city on its reconstruction journey, or at least the cities with the worst damages, it would help to ensure that no communities were left behind. This is not a small ask, but these partnerships can begin with small financial commitments and focus on highlighting local needs across Ukraine’s forgotten municipalities for the international donor community. EIB developed a unique solution to the difficulties of local governments’ creditworthiness and the fact that some needs may be too small for the major loan providers, which could be replicated by other major funders: financing guaranteed by the European Union in sovereign loans. In many cases, receiving aid comes down to how well the local leadership can energize international supporters. However, most mayors don’t have the capacity to advocate for their cities on the global stage—in some cases because of simple language barriers but also because of poor creditworthiness.

Large state-owned enterprises also require credit instruments tailored to Ukraine’s exceptional circumstances and needs. This implies intense coordination among those in development finance who are willing to take on the challenge. In June 2023, the EBRD—the largest institutional investor in Ukraine—and eighteen other development finance institutions signed a memorandum of understanding (MoU) on a Co-investment Platform to support Ukraine’s SOEs and private sector. In practice, this means the institutions are meant to coordinate their activities so that funding is deployed strategically. Participants held their first meeting following the MoU in Norway in May 2024.

Where will next year’s money come from?

The outlook for financial assistance to Ukraine is now adequate—a reversal of fortune since the cash-flow challenges in February. It is crucial to avoid making the same mistakes that led to this crisis, which forced Ukraine’s government to slow the pace of even basic repairs.

The European Union and the United Kingdom have made multiyear commitments: £3 billion in the United Kingdom’s case and—assuming the European Union sends at least one-fourth of its four-year Ukraine Facility budget—€8 billion in loans and €4.25 billion in grants from the European Union. On the other hand, the IMF’s disbursements will slow from $5.3 billion to $1.8 billion and most other IFI commitments will go to infrastructure projects and private firms, not the central government. We also have seen that Ukraine’s private bondholders are pushing for interest payments to start again.

As the war draws on, it also seems likely that expenditure will have to be bigger than currently forecast—by about $12 billion above the current baseline deficit projection of $23 billion.

So what can be done?

Recent G7 discussions about using the future interest income from the approximately $300 billion of Russia’s reserves immobilized in the West to lend funds to Ukraine are showing more promise than they have before. The solution would offer a timely injection of cash, $50 billion or more, and this wouldn’t preclude any long-term policy involving the reserves.

The full amount won’t be transferred to the government of Ukraine in one go and it is highly likely some of it would be used to buy weapons on Ukraine’s behalf. Nonetheless, to finance a gap in the 2025 budget which could be the $10-12 billion normally financed by the United States, the instrument could be very useful indeed.

The details that still need to be ironed out for the loan to work include the risk sharing between Europe and North America.

Demining and air defenses should be more of a priority

The international community has not fully grasped the scale of demining that needs to take place in Ukraine, particularly in the liberated territories, to make them ready for reconstruction. Mine contamination and other explosive hazards riddle over a third of Ukraine (180,000 square km), according to the Ukraine government, endangering civilians, halting agricultural activities, and detracting from such areas’ investment prospects. It also complicates the return of civilians to the liberated territories. However, with the right resolve and the latest technologies, Ukraine’s allies can remove this large-scale obstacle to reconstruction.

Ukraine’s National Mine Action Authority, which was established under Ukraine’s 2018 Mine Action Law, oversees mine action activities, coordination, monitoring, and tasking and is in charge of approving national plans for mine action. The Mine Action Centre (under the Ministry of Defense) organizes and coordinates demining efforts in Ukraine, which are conducted by the State Emergency Service of Ukraine, and works with the Humanitarian Demining Center. The Ministry of Economy and the Ministry for Reintegration of the Temporarily Occupied Territories of Ukraine also lead land mine clearance efforts.

The United Nations Development Programme (with contributions from several Western nations) funds 80 percent of the demining operations and multiple nongovernmental organizations such as the HALO Trust are present on the ground. Direct bilateral donations, technical support, and equipment assistance also play crucial roles. The United States, the European Union, and South Korea, among others, have made important in-kind donations with innovative systems including MV-10 demining systems. External entities sometimes struggle or take a while to receive accreditations to assist in demining, but their role is essential. Streamlining the process also offers an opportunity to engage countries and organizations that have been unable to provide military support for Ukraine, like Ireland.

Compared to demining, the lack of air defenses receives relatively more coverage—precisely because the situation has become steadily worse since late 2023. Facing off against Russia’s inexpensive kamikaze drones, Ukraine’s rate of success with its air defenses remains high at 82 percent, but the frequency and sophistication of attacks—often starting with fleets of drones and followed by ballistic missiles—are designed to overwhelm systems. A lack of provision from allies has forced Ukraine to use its supplies sparingly so even valuable economic assets have to be knowingly sacrificed, like the Trypilska power plant in the supposedly well-protected Kyiv region.

The supplemental passed by the US Congress will restore some supplies—but other initiatives including a German-led effort to donate Patriot batteries have fizzled. Finding solutions is beyond the scope of this report, but we see the damage done to Ukraine’s energy network and economy and would welcome anything that can spare Ukraine the impossible dilemma of not being able to shoot down a cheap missile that wreaks extremely costly damage. Analysts have suggested that Poland, for instance, should protect its border areas by shooting down Russian missiles in Ukraine’s skies that are adjacent to its air space, which would free Kyiv to focus its resources further east. Others have suggested embracing Ukraine’s ability to target drone production facilities, storage, and launch units in Russia.

Empowering Ukraine’s leadership structure for success

The chain of command for economic recovery and reconstruction is understandably split and subject to change. As the Office of the President reorganizes these authorities, the priorities should be easy engagement and transparency. Currently, the bodies in the executive branch that have a say over these issues include the Cabinet of Ministers as well as the Ministry of Economy, the Ministry of Energy, the Ministry of Strategic Industries, and last but not least, the Ministry for Communities, Territories and Infrastructure Development. Created by a merger of two ministries in December 2022, the latter oversees the State Agency for Restoration and Infrastructure Development. In the coming months, this key ministry is likely to be split again into separate ministries for regional development and infrastructure.

Meanwhile, the dismissal of the top team at the soon-to-be divided ministry met with some consternation. The team was known for its commitment to transparent decision-making and open data: The DREAM platform was one of its most recognizable achievements. At the June Recovery Conference in Berlin and over the second half of the year, it will therefore be fundamental for the government to show that the systems (and the principles behind them) remain central to decision-making on the allocation of funds to projects. The same should go for procurement. The ProZorro portal, Ukraine’s e-procurement system, is not being used for any military spending, although this represents half the government’s budget. It should be possible to set tenders on nonsensitive purchases through this system.

A second gap concerns the management of big-ticket investments that will drive Ukraine’s modernization and its integration into the EU single market. Ukraine needs an updated public investment management framework and also a fit-for-purpose vehicle for private-sector stakeholders—including those with little to no exposure to Ukraine—to interact and agree on joint ventures. One goal of the Berlin Recovery Conference is to create an online platform for this—which notably could provide access to insight on the relative war risk and mitigation strategies. For it to work, however, the methodology will have to be agreed at least between the government of Ukraine, the European Union, and the IMF, and discussions are ongoing. Once running, this platform should not be restricted to firms based in the participating countries of the Multi-agency Donor Coordination Platform. While these capitals may feel they deserve some recompense for their efforts, it would be foolish to exclude firms that are interested and have something to offer. The most obvious example: Turkish building contractors, who represent the second-biggest global force in this sector after China, provided they aren’t servicing the Russian market.

Section 3: Steps to create a reconstruction-friendly ecosystem

The pull of EU accession

It was the Euromaidan protests against the Ukrainian government’s failure to sign an Association Agreement with the European Union in 2013—as President Viktor Yanukovich pivoted toward Russia—that led to the 2014 fall of the government in Kyiv. Russia responded by invading Crimea and southeastern Ukraine, violating Ukraine’s territorial integrity. Ukrainians continue to desire EU membership, seeing in it the promise of a more prosperous and stable life, and are overwhelmingly in favor of moving in this direction.

The EU accession process is demanding—and provides a very useful framework for reform, with clear incentives, visible and embraced by the public, for making progress toward EU standards.

The thirty-five chapters of the acquis—the body of common rights and obligations that is binding on all EU member states—all come with dozens of reforms. Firms based within the EU’s current border represent an important driver of the move to higher standards in anticipation of membership. Invaluable transfers of know-how on EU law compliance can happen as long as there is a sense that the government and the parliament are stewarding the reforms through.

Even with the uncertainty of the war, tapping into such virtuous cycles will be vital. Efforts made now to comply with environmental standards in the short term will shorten the wait for EU accession. All mid-term reconstruction planning should account for sustainability and green elements and, while there is a minimum threshold of 20 percent of these in the Ukraine Facility, it is worth identifying which will have the maximum impact on Ukraine’s carbon emissions.

Ukraine’s National Energy and Climate Plan (NECP) for 2025-2030 is in line with 2030 Energy Community Treaty energy and climate targets. However, there will be several areas where a long-term vision for Ukraine’s economic and societal prosperity must be carefully balanced with the most urgent wartime needs to keep the lights on, the government running, and the economy afloat. With the latest bombardment on Ukrainian energy generation, securing gas turbines and multiple co-generation facilities and fixing coal power plants must be prioritized in the immediate term. This does not amount to reducing the roles of renewable energy, efficiencies, and clean technologies deployment: Ukraine’s government drew from a clean energy road map produced for Kyiv by nine US agencies ahead of the UN COP 28 climate talks as it set its decarbonization goals, while finalizing its recovery and energy strategy. But a big concern is just what kind of price Ukraine could pay when the European Union’s Carbon Border Adjustment Mechanism (CBAM) kicks in in 2026, with tariffs that penalize trade from countries with insufficiently rigorous environmental rules. The European Union should bear in mind Ukraine’s wartime context. A 2023 European Commission staff report notes Ukraine’s “good progress on environment, some progress on energy and Trans-European networks,” and limited progress on climate change and transport policy.

The European Union, recognizing how cumbersome accession can be, has identified sixty-nine priority reforms, most of which are tied to investment indicators. Some Ukraine Facility disbursements will be tied to progress on these, providing added incentives for progress along the way toward the long-term goal of EU accession.

At this early stage, we are concerned about the European Union’s ability to keep offering Ukraine advantageous market-access terms: They have helped generate much-needed cash for Kyiv and almost all regions, but the objections of European farmers and truck drivers can’t be ignored. As part of the association agreement, the EU-Ukraine Deep and Comprehensive Free Trade Area allows for tariff-rate quotas if a particular good is being exported in excessive amounts. Yet more elegant solutions exist, especially with fungible products like food. More grain entering the single market should also mean the EU has more capacity to export, and global demand remains high. EU and national leaders should be bolder in calling out and refuting Russian disinformation meant to exploit such issues.

Still, the Polish farmer border protests are symptomatic of a wider challenge that the European Union and Ukraine will have to face together. Ukraine remains much poorer than even the least well-off EU member states. In this European Parliament campaign season, low wages in Ukraine have frequently been invoked by some at the political extremes as a reason to delay or refuse Ukraine’s accession. And if the rules on cohesion funding were left unchanged, the EU Council estimates that €186 billion would be redirected to Ukraine over a seven-year budget cycle at the expense of “convergence” elsewhere in the bloc. The European Commission is already working on how it will have to change the rules, but the task is momentous—and will inevitably be costly. An underused argument which Kyiv and EU capitals should lean on more often is that, with the right reforms, Ukraine’s joining the single market can be a net contribution to Europe’s strategic autonomy. We shall see in the following section just how much Ukraine has to offer, from food and critical raw materials to battle-hardened know-how on defense and IT.

Decentralization and winning the fight against corruption

Ukraine has a successful track record on decentralization. Starting from a low bar in the aftermath of the Revolution of Dignity, Kyiv embarked on a three-year process to rebalance decision-making. A new status for amalgamated municipalities, or hromadas, was created and revenue for local authorities increased threefold through a combination of direct transfers and new tax-raising powers. The new hromadas have played a vital role in assisting citizens throughout the war, and they are mostly ready to help allocate funds to reconstruction projects in a way that best suits their citizens.

One area of reform that was incomplete before the 2022 invasion was providing hromadas with the ability to act as a “legal person.” This would provide them with the ability to borrow money more easily and make claims through the courts in a more reliable way. Completing this reform should clearly be a priority so that hromadas can take on a fuller role, including by actively raising funds.

On our research trip, we heard differing accounts of how the anticorruption apparatus was faring. On paper, the division of labor is straightforward and justified. The National Agency on Corruption Prevention (NACP) takes care of strategy and foreseeing legal bottlenecks in dealing with corruption. The Specialized Anti-Corruption Prosecutor’s Office can launch investigations, and the High Anti-Corruption Court’s role is self-explanatory. The National Anti-Corruption Bureau of Ukraine (NABU) has a much broader role, and interlocutors ranging from elected legislators to business leaders suggested this may have become a little too wide-ranging and could do with more checks and balances. It is clear that Ukraine needs a transversal body that is independent and can withstand political pressure. NABU would do well to pursue this important work without television cameras in tow for showy raids and arrests, which only play into Russian propaganda on corruption in Ukraine.

The corpus of judges in Ukraine needs new recruits. The overhaul of the political class since 2014 has not been accompanied by the same replenishment in the judiciary and courts rank among the least trusted public institutions in the country. To the government’s credit, the war has not slowed longstanding plans to “liquidate” the most notoriously corrupt courts, like the District Administrative Court of Kyiv, but the new bodies being set up are often staffed by the same people.

Energy sector reforms

Energy sector reforms have a dedicated subsection in this brief due to their outsized impact on Ukraine’s broader economic recovery.

Tremendous progress has been made on governance and institutional reforms, anticorruption measures, rule of law, and human rights. However, the war has posed unique challenges and opened the door to backsliding, something that had made private equity stay away even before the full-scale invasion. When institutional investors and companies consider entering the Ukrainian market, war risks are not the only deterrents. In addition to concerns shared by other investors about judicial independence and capital controls, energy sector investors seek assurances against seizure and/or nationalization of their assets, whether their return on investment can be easily taken out of Ukraine without controls or restrictions, and whether board management is independent and fully functional.

It will remain challenging to convince foreign investors that Ukraine’s energy sector is worth the additional risks when similar returns could be secured elsewhere.

Good arguments exist. Entering Ukraine’s market now, before reconstruction picks up speed, would give companies competitive advantage and valuable market insight, while paving the way for other growth opportunities in the region.

Ukraine has also conducted energy reforms. The Cabinet of Ministers adopted a resolution on the guarantees of origin for electricity generated from renewable energy sources. This legislative change will improve transparency and valuation of renewable energy production for accurate feed-in tariff payments and cross-border exports, particularly as the European Union works toward expanding the CBAM’s scope. Additionally, Ukraine adopted reforms to align its legislation with the EU Regulation on Energy Market Integrity and Transparency, which drives wholesale energy market integrity and transparency and combats market manipulation with help from an independent utility regulator, the National Energy and Utilities Regulatory Commission, adopted in May 2023.

Another huge milestone is Ukrenergo’s full membership in the European Network of Transmission System Operators for Electricity, as of January 2024, two years after Ukraine cut ties with Russia’s electric grid and pivoted to the European network in record time. Thanks to the updated EU Trans-European energy network regulation, Ukraine can apply for project funds through the Connecting Europe Facility (CEF) program’s calls for transport proposals to strengthen connectivity with EU member states; moreover, the status of the projects of mutual interest may unlock funding and streamlined permitting for energy infrastructure. Cross-border renewable energy projects offer yet another avenue for Ukraine to pursue CEF-Energy support.

Nonetheless, the energy sector has more work to do, particularly in moving toward liberalization of electricity prices. Although an extremely unpopular reform, charging market rates for the cost of electricity would reduce debt for Ukraine’s national energy companies, incentivize efficiency solutions, and attract foreign investment when developers can rely on receipt of payments for electricity generation and services. It’s important to note that ending the blanket fixed low electricity prices for households would be particularly challenging when households are barely getting by. However, with carefully targeted support for consumers in need and effective communication strategies with grassroots engagement, Ukraine can take this difficult step toward creating an attractive investment environment. Extra care must be taken to ensure that this reform does not affect energy security or access for the Ukrainian population, particularly the elderly and disabled, and those with financial hardships or other obstacles. Several waves of tariff increases have already taken place, driven by the financial strain of repairs needed across the system: Prices nearly doubled in June 2023 and again in June 2024. However, they are still below the market rate. Ukraine needs to develop a timetable for the careful phaseout of public service obligations, paired with robust strategic support for the most vulnerable consumers. In addition, Ukraine has opportunities to reduce consumption across district heating systems and integrate efficiency criteria into public procurement processes.

War risk and political risk: Insurance mechanisms

Ukraine was a very large market for “war insurance”—until the war. In February 2022, the risk of an insured asset being damaged became too high for private providers to be able to provide new insurance at a competitive price, and the market dried up. Laudable progress has since been made.

State backing was extremely helpful for insuring the first Black Sea convoys, under the UN-brokered grain initiative. Now, the risk is better spread between friendly governments and a nascent market. The World Bank Group’s Multilateral Investment Guarantee Agency (MIGA) can issue trade finance guarantees giving exporters and logistics providers peace of mind that they will be compensated for shipments that don’t make their destination.

While the available insurance products are a big achievement, they only offer coverage for as long as the shipment lasts. Long-term insurance covering the private investments Ukraine needs is scarcely available. The World Bank’s MIGA has provided coverage for new warehouses and the Unites States Development Finance Corporation and Poland’s Development Fund offer guarantees against political and war-related risks as well. Still, Russia’s targeting of economic assets make an insurance market capable of covering high value-add installations a remote possibility for now. It is still important to prepare. Building robust data portals for evaluating risks and differentiating for every region can start to build an appetite for the private sector to reenter the market.

Human capital

Ukraine’s greatest reconstruction asset is its human capital—and also its most concerning shortage.

Ukraine’s labor markets have been through tremendous disruption since the onset of Russia’s full-scale invasion, with a massive loss of jobs followed by labor shortages in some sectors and high unemployment in others. As men get called to the front lines, women make up a larger percentage of the workforce. Automation and other efficiencies happen out of necessity.

Nonetheless, Ukraine needs to continue making progress on merit-based recruitment and reforming job classifications and salaries because transparency and human resource management feature among the sixty-nine priority reforms in the Ukraine Facility Plan, which calls for a “transparent procedure for selecting specialists for positions and digitalization of civil service and human resources management.” These are major issues for the public and private sectors.

Human capital will play a disproportionately large role in the success of the recovery efforts, which means that investments today will bring compounded economic benefits down the road. Creating a path for bringing people back to Ukraine now—through lucrative employment opportunities, secure schools, and robust air defense capabilities—will be vital for a successful economic recovery and, eventually, self-sufficiency.

Reintegrating veterans into civil society and the workforce is both an economic and societal imperative for Ukraine, and there could be five million of them by the end of the war. Some have missed out on higher education due to the war and should be supported in advancing their studies, should they choose to do so. Others may seek upskilling or retraining. But their unique postservice needs must be prioritized first, with easy access to services including healthcare and financial support.

Ukraine’s future workforce includes schoolchildren now living close to the front lines and who are losing years of schooling due to the insufficient number of shelters. This is the biggest impediment to continued education, as Russia targets kindergartens, schools, sporting facilities, and libraries in its ruthless campaign. Donors should prioritize building shelters to optimize children’s educational opportunities and future career prospects. Big City Lab, in collaboration with public and private stakeholders, is developing principles and testing out pilot projects on how to most effectively rebuild and remodel old Soviet school buildings into safe, social, multifunctional, and innovative spaces fit for tomorrow’s needs. Such pilot projects can be recreated in other sectors to develop best practices for reconstruction.

International organizations can expand support for strategic reskilling, upskilling, and specialty trade training. The technology sector can provide the mechanism for these trainings and is a growing sector in its own right, particularly in providing employment opportunities for veterans. Digital startups are at the front lines of innovations. Ukraine is already exporting solutions, such as the Diaa portal of digital services, to other countries.

Rail, roads, and ports

Efficient and frequent movement of goods will be a key metric for Ukraine’s economic recovery.

And to reinforce earlier points, none of these large-scale investments will be realized without sufficient and sustained air defense. Investing in Ukraine’s transportation system by the EBRD, EIB, and the World Bank must be scaled now through private sector engagement to maintain current trade volumes and prepare the system for large-scale reconstruction efforts, including the tonnage of materials coming in and burgeoning exports leaving Ukraine through ports, railways, roads, and air.

Ukraine has already achieved important transportation reforms, such as decentralizing the state agency of roads, Ukravtodor, and reforms and greater transparency through ProZorro. However, Ukraine will need to adopt and implement the trans-European transport network (TEN-T) guidelines and prepare its transport system for decarbonization and digitalization.

Donors have an opportunity to support feasibility studies for priority projects identified under the Indicative TEN-T Investment Action Plan. Moreover, pairing ProZorro with additional transparency and verification measures in the transportation development area will contribute to weeding out corruption risks and instilling confidence for the donor community. Digitalizing, upgrading, and securing “soft infrastructure” like customs controls and port data systems would improve efficiency and ensure consistent adherence to process.

The US government deserves particular praise here. USAID’s contribution to upgrades to border crossing infrastructure and railway infrastructure leading to the European Union will help the integration of Ukraine’s economy into the single market; and while a prosperous Ukraine is clearly a US foreign policy goal, the projects will benefit the US economy much less directly.

Section 4: The best opportunities for each economic sector

Russia’s hybrid war is spreading at the rate of an aggressive cancer, penetrating all sectors of Ukraine’s economy to destroy Ukraine on the financial battlefield, as Russian President Vladimir Putin fails to win on the actual front lines. Every dollar Ukraine can produce through trade is a win against Moscow’s efforts to diminish Ukraine’s economic output, and vital tax revenue for the military budget. Support for Ukraine’s top sectors and trade is the smartest investment into the country’s future self-sufficiency and economic stability.

The European Council presidency, in consultation with parliament negotiators, provisionally extended the duty-free trade agreement with Ukraine until June 5, 2025, which is pending June steps for official adoption. The action—which includes an automatic safeguard mechanism to trigger “tariff-rate quotas” for poultry, eggs, sugar, oats, maize, groats, and honey as well as “enhanced monitoring” of wheat and cereal imports—underscores the importance of EU member nations’ domestic communication of the benefits of this economic lifeline for Europe.

Recovery Priority #1: Supporting Ukraine’s energy sector

The energy sector will be the engine of Ukraine’s reconstruction, but urgent support is needed now to keep it from collapsing. Moscow annihilated much of Ukraine’s energy generation—but not the country’s rich energy potential, nor its ingenuity and resolve. Ukraine urgently needs more air defense and a lifting of restrictions on how it deploys weapons furnished by its allies to prevent Russians from leveling more cities and driving civilians into a state of despair and displacement. As long as any prohibition to use US weapons for attacks on Russian soil is in place, Ukraine’s power plants are sitting ducks and prime targets for Moscow’s bombardment. These restrictions are slowly and incrementally being lifted, but Kyiv still faces difficult trade-offs on defending key economic assets.

Ukraine’s air defense and offensive capabilities should be complemented with passive protection (i.e., physical barriers for critical infrastructure) which is effective against drones and is currently being enhanced to withstand missiles when covering smaller critical structures such as a transformers, substations, and generators. Meanwhile, the large power plants must rely on air defense for protection. This multilayer strategy for defending critical energy infrastructure—grid, centralized power plants, transformers, gas storage systems—is crucial for future energy development and energy system transformation.

The latest wave of attacks aimed at destroying centralized energy production capacity and natural gas storage caused immeasurable harm and system imbalance, with Ukraine having to resort to scheduled blackouts and purchasing electricity from its neighbors instead of producing it at home at a fraction of the price. Preparations for the winter must start now as the system is already in critical condition months ahead of the heating season. Securing and financing gas turbines to ensure sufficient capacity and balancing the grid is a matter of life and death for the Ukrainian population this winter. The G7+ Energy Coordination mobilizes efforts to restore and protect Ukraine’s energy infrastruture through efforts such as equipment procurements and the Ukraine Energy Support Fund, managed by the Energy Community Secretariat, is intended to finance critical energy equipment for Ukraine, such as procuring gas turbines. All possible efforts must be made to expedite procurement while adhering to the Austrian Federal Public Procurement Law (given that the secretariat is based in Vienna). Capacity-driven delays must be addressed through proper staffing at the secretariat and timely communication with the Ukrainian stakeholders.

Decentralizing Ukraine’s energy production system requires a multipronged strategy, which Ukrenergo is leading with support from relevant ministries. Distributed generation would advance decarbonization, make for challenging targets for Moscow’s attacks, and could present an appealing investment opportunity for the private sector. Such a system will require smart and digital solutions and customer service, with strong cybersecurity measures. Storage installation could be owned by the distribution system operators to attract financing. Coordination with local communities, both to tap their capacities and get buy-in, will be foundational to the success of building out distributed networks. Ukraine can work towards establishing a decentralization ecosystem through regulatory changes (such as streamlining connectivity rules), feasibility studies for projects, and liberalization of electricity prices.

Ukraine has tremendous clean energy resources (including wind, solar, hydropower, and geothermal potential); low-carbon gases including biomethane; critical minerals deposits; and unparalleled expertise in cybersecurity and system resilience and recovery from kinetic attacks. Conducive policies will be essential for encouraging investments. Ukraine’s National Energy and Climate Plan—an important condition for securing financing via the EU’s Ukraine Facility—will be presented at the Berlin Recovery Conference on June 11-12: This will signal which clean energy technologies will play the biggest roles in meeting climate targets for the country, the policy gaps to enable their deployment, and most importantly, private investment needs to reach scale.

There is untapped potential in energy efficiency for Ukraine. Soviet buildings were built without care for energy conservation. Determining which buildings to remodel and which to demolish will be an important part of the reconstruction process. Cost and building condition will play a major role. The industrial sector presents tremendous opportunity for cutting energy consumption and could lead to 12.5 million tonnes in CO2 reduction, and $3 billion in annual savings, with $13 billion in investments through 2030. Low energy costs are also a key driver in industrial competitiveness and would contribute to the revival of this important sector. In 2023, Ukraine launched the State Fund for Decarbonization and Energy Efficient Transformation, which could be an effective mechanism for attracting international loans and grants for the implementation of investment projects. However, Ukraine will need market mechanisms to properly account for the value of energy efficiency investments, which pay for themselves over time (particularly in a liberalized market), but may require a higher upfront cost compared to less-efficient construction and technologies. For scale, Ukraine will need market solutions which will enable the private sector to capitalize on efficiency investments. On paper, Ukraine’s energy efficiency rules are generally aligned with the European Union’s; however, opportunities exist for infusing energy efficiency criteria into both the public procurement process and strategy for building renovations. Ukraine should also seek to attract investment for making the transmission and distribution systems more efficient.

A number of Ukrainian state-owned enterprises, such as Energoatom and Ukrnafta (owned by Naftogaz), are integrating independent boards into their leadership structure to create additional layers of transparency and verification. These boards will have a unique opportunity to advance implementation of reforms and instill confidence through transparent operations and practices.

Nuclear energy is a critical low-carbon, balancing resource for Ukraine, which has a wealth of expertise in the sector. Ukraine should continue building partnerships with Western countries and companies to extend the life of existing reactors, build out new capacity, and diversify nuclear supply chains for future nuclear plants and uranium enrichment. To lay the foundation for an appealing investment environment, Ukraine needs to complete reforms at Energoatom (under the leadership of the new supervisory boards) and carve a path forward on transparent denationalization. Following debilitating capacity losses, Ukraine is looking to undertake nuclear build-out starting as early as 2024, utilizing existing equipment from Bulgaria. Most importantly, the international community must pressure Russia to leave the Zaporizhzhia nuclear power plant, a 6 GW facility, before an accident takes place.

Recovery of Ukraine’s energy sector will hinge on the support of a multitude of stakeholders, and multilateral development banks are poised to play a key role. When it comes to gas, however, some of these institutions have guidelines that prevent or make it challenging to finance such infrastructure, per climate commitments. This is a missed opportunity to support Ukraine in its time of need—especially since investment in gas turbines and piston installations would accelerate Ukraine’s shift away from coal.

Ukraine’s natural gas network could be redeployed to transport Ukraine’s indigenous gas production and low-carbon gases (with some adjustments), after the gas transit agreement with the Kremlin expires by the end of 2024. There is a chance that European traders may work out a short-term agreement with Gazprom on the flows and negotiate the transit fees with Ukraine separately. However, for any gas flows to continue moving through Ukraine, the country needs to invest in border-metering mechanisms for clarity on export volumes. Ukraine also needs a strategic vision for its robust pipelines network, most of which is not utilized at the moment, as the upkeep of the entire network weighs on the country’s expenditures at a critical time. With sufficient air defenses, European traders can continue to utilize Ukraine’s vast gas storage in the western part of the country—which they have done so far without war risk insurance. The storage system has demonstrated incredible resilience in light of the recent escalatory attacks.

Large-scale investing in agriculture

Dodging bombs and navigating land mines are not standard farming practices, yet Ukrainian farmers have persisted. The resilience and bravery shown in this sector, which employs 14 percent of Ukraine’s population and yields 12 percent of country’s GDP, must not be taken for granted. The sector requires large-scale investments to continue and expand this level of production and prevent famine for the consumers reliant on Ukrainian crops, who number 400 million.

First and foremost, Ukraine’s farming communities must be demined (as discussed above), and secure and reliable transportation routes and storage must be established.

The full liberalization of the agriculture market in early 2024 unlocked a variety of financial mechanisms for farmers, such as the ability to borrow against their land. Notwithstanding, additional capital is needed for farms of all sizes to improve operations productivity and maintain export levels.

Avoiding deindustrialization and seeking a competitive edge in manufacturing

Ukraine’s manufacturing sector has been battered since Russia’s initial invasion in 2014, which led to illegal occupation of Ukraine’s industrial centers. COVID-19, inflation, the full-scale invasion, and workforce migration (mostly forced by the war’s atrocities) have placed more pressure on the neck of once a robust economic sector. Massive investments in modernizing, digitalizing, and efficiency measures are needed to keep Ukraine’s factories afloat. But the sector is also deeply interconnected to developments in air defense, secure and reliable transportation routes, transparent and functioning customs systems, and clear signals from the European market on how Ukraine can contribute to EU strategic autonomy through priority trade partnerships such as in the mining and processing of critical minerals.

Unleashing tech innovations

Ukraine is digitizing its economy at record speed. In some cases, this is happening out of necessity to provide vital, urgent services in a safe environment through platforms such as DREAM, Diaa, Prozorro, and United24. Digitalization also enables transparency and verification—top requests by Ukraine’s donors. This is also a space with top growth potential as new sectors integrate digitalization into their reforms and to create efficiencies and automation. Ukraine’s sophisticated IT sector offers some of the most desirable jobs in the country, with one opening attracting 150 applications. The sector already employs 300,000 professionals and has plenty of room to grow. Ukraine has a unique opportunity to unleash its digital space innovations while it prepares to synchronize its regulatory environment with EU legislation such as the Digital Services Act, AI Act, and the Digital Markets Act.

Summary of recommendations

Measuring the damage

International stakeholders

- Support Ukraine’s capacity to track damages, develop a verification mechanism, and connect to resources, particularly in areas that may lack capacity and capabilities with documenting destruction. Enlist AI and automation where feasible.

- Develop a focused platform enabling the Ukrainian government and IFIs to differentiate among large-scale projects as either long-term or short-term/urgent repairs.

General reconstruction strategy

International stakeholders

- Provide multiyear financial, recovery, and military assistance commitments (of five years at a minimum) to establish a reliable investment ecosystem.

- Support reconstruction during wartime as a vital ingredient to Ukraine’s victory, morale, and future economic prosperity, treating this call for international investment with the urgency necessary for its success.

- Unify around an allied vision and approach toward Ukraine’s reconstruction to ensure efficient resource utilization and impactful collaboration.

- Prioritize support for the completion of demining Ukraine’s territories to avoid derailing reconstruction.

- Enhance aid and reconstruction coordination efforts among donors via the special envoys for reconstruction.

- Support municipalities and underserved communities in advocating for themselves through, for example, partnerships between European nations and Ukrainian cities, following the success of the Denmark-Mykolaiv example.

- Find creative financial solutions for local government authorities and SMEs which lack creditworthiness, using sovereign guarantees and workarounds provided by the EIB where possible.

- Recognize the delicate balance between Ukraine’s urgent needs to fuel the economy and making progress toward a resilient, low-carbon future.

- Make recovery convenings more impactful through an action-driven approach.

- Continue decoupling from Russian infrastructure.

- Encourage CEOs and boards to visit Ukraine to understand the challenges and opportunities.

Ukraine government

- Enhance the leadership structure of and coordination across Ukrainian ministries, streamlining decision-making and communication with external stakeholders.

- Kyiv should continue building out trust and transparency mechanisms to showcase how international support is deployed.

Energy sector

International stakeholders

- Assist Ukraine in bolstering protection of its energy infrastructure, which needs passive (physical barriers) and active (air defense) protection from Russian bombardment to minimize future damage and attract investment in the sector.

- Expedite equipment procurement under the Energy Community Secretariat platform and other mechanisms.

- Participate in public-private investments to advance decentralization of the energy network through distributed generation, batteries, and prosumers (i.e., those who both produce and consume energy), which is a massive undertaking necessary to secure, decarbonize, and liberalize Ukraine’s energy system.

- Reduce barriers and restrictions for multilateral development banks to finance gas infrastructure in Ukraine to secure sufficient capacity and balancing services this winter.

Ukraine government

- Devote vigor to the important work of decentralizing the energy network.

- Make progress on liberalized energy market pricing while maintaining targeted subsidies for vulnerable populations.

Agriculture

International stakeholders

- Invest in demining, transportation, and storage.

- Ensure farms of all sizes have access to capital.

Workforce

International stakeholders

- Prioritize building school shelters to optimize children’s educational opportunities and future career prospects.

- Expand support for strategic reskilling, upskilling, and specialty trade training opportunities.

Ukraine government

- Continue to make progress on merit-based recruitment and the reform of job classifications and salaries.

- Support veterans in reintegrating into civil society with comprehensive services, continued education, and reskilling and upskilling opportunities.

Finance

International stakeholders

- Support Ukraine in absorbing aid in a timely manner through capacity building and streamlined procurement.

- Promote Ukraine’s potential as a net contributor to Strategic Autonomy. EU citizens tend to be told about substantial cost of supporting Ukraine’s accession but know less about its supplies of critical minerals (especially titanium) and its innovative defense sector.

- Unlock grants and incentives for Ukraine’s private sector, particularly in workforce development and creating efficiencies and automation. Provide support for small- and medium-sized enterprises through grants, loans, and risk mitigation, addressing the main barrier of war-related risks and the lack of related insurance products.

Ukraine government

- Continue to modify strict capital controls imposed at the beginning of the full-scale invasion, which are a deterrent for new investors. A recent relaxation announced by the National Bank of Ukraine includes a provision for the payment of dividends to foreign investors and the repayment of foreign currency loans, albeit under a monthly cap, which should be gradually lifted as long as capital outflows do not undermine financial stability.

Stakeholders and the Ukraine government

- Ensure that no communities are left behind during aid distribution through municipalities capacity building.

General reforms

- Complete the decentralization reforms, including granting hromadas “legal person” status.

- Hire new judges and improve their salaries.

- Harness investment by firms based in the EU as a driving force for convergence with EU rules and norms.

Conclusion

This report has avoided sugarcoating the reality of Ukraine’s economic and financial predicaments. We still believe it is a testament to unmatched resilience and innovation amidst the challenges of war. As we discuss recovery, two imperatives emerge: sustained multiyear military support, especially for air defenses; and clear, forward-looking funding commitments, in macro financial assistance and in recovery grants and loans. These are two distinct funding streams but, when we visited Kyiv, uncertainty over the former was affecting the government’s cash flow and preventing it from focusing on recovery projects which were already feasible.

Even amid conflict, reconstruction is necessary because of the destruction it has wrought. By prioritizing viable projects in sectors such as energy, industry, agriculture, transport, and technology, and ensuring transparency, we can drive economic recovery and help Ukraine meet EU standards.

The upcoming conference in Berlin has broken the task ahead into four dimensions: business, the human dimension, regions, and EU accession. However, due to Russia’s ongoing attacks, the most urgent priorities are restoring energy capacity and bolstering air defenses to protect new and existing assets.

Now is the moment for Ukraine’s allies to take decisive action. By supporting Ukraine today, we invest not only in its survival but also in its future contributions to a stronger, more prosperous Europe. Together, we can help Ukraine rebuild and thrive, setting a powerful example of hope and resilience for the world.

ABOUT THE AUTHORS

The authors would especially like to thank Nicholas Pantazopoulos, who conducted critical graphing and cartography, and Lizi Bowen, who led web design, in this effort.

RELATED CONTENT

At the intersection of economics, finance, and foreign policy, the GeoEconomics Center is a translation hub with the goal of helping shape a better global economic future.

The Global Energy Center develops and promotes pragmatic and nonpartisan policy solutions designed to advance global energy security, enhance economic opportunity, and accelerate pathways to net-zero emissions.

The Eurasia Center’s mission is to enhance transatlantic cooperation in promoting stability, democratic values and prosperity in Eurasia, from Eastern Europe and Turkey in the West to the Caucasus, Russia and Central Asia in the East.

Image: A sapper of the State Emergency Service pulls an anti-tank mine as he inspects an area for mines and unexploded shells, amid Russia's attack on Ukraine, in Kharkiv region, Ukraine March 21, 2023. REUTERS/Viacheslav Ratynskyi